What about the 12% of simulations that show the US debt-to-GDP ratio is on a sustainable path?

What about the 12% of simulations that show the US debt-to-GDP ratio is on a sustainable path?

Unsustainable path means an increase in the US debt-to-GDP ratio, according to Bloomberg Economics

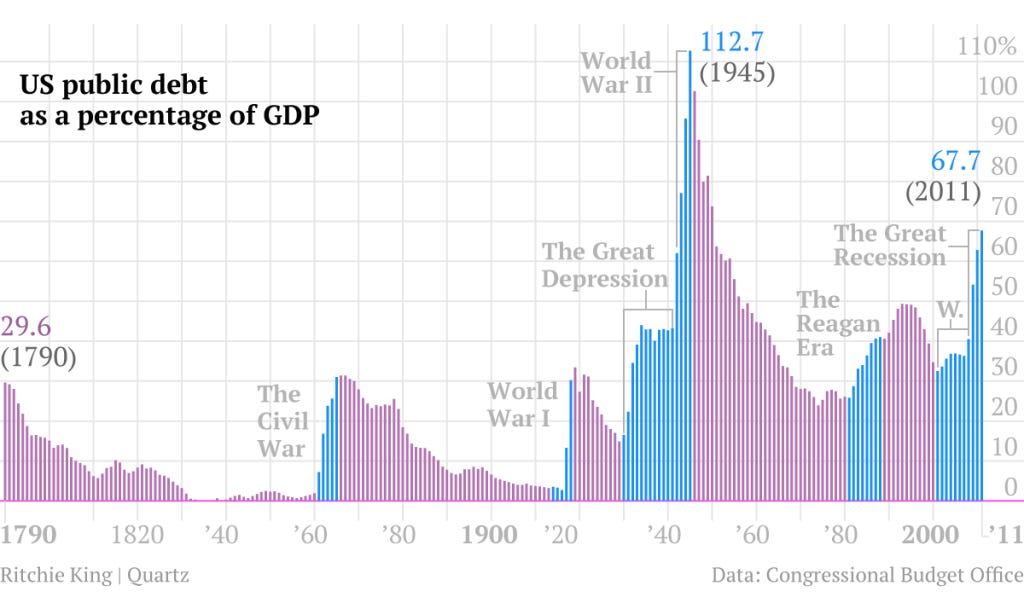

The Congressional Budget Office projects the US debt-to-GDP ratio to grow from 97% in 2023 to 116% by 2034. For perspective, the US debt-to-GDP ratio during World War 2 was 116%, the highest debt-to-GDP ratio that the US has experienced. While the chart below is from 2012, add the tax cuts, the new wars that occurred, and the pandemic and the chart will look worse.

Since forecasting the US debt-to-GDP ratio comes with many variables, Bloomberg Economics ran a million simulations to predict the likelihood that this ratio will increase. As Bloomberg noted, “[i]n 88% of the simulations, the results show the debt-to-GDP ratio is on an unsustainable path - defined as an increase over the next decade.” From that, I wondered why 12% of the simulations showed the debt-to-GDP ratio on a sustainable path.

Historical Context on why these ratios have declined

To understand how we can lower the US debt-to-GDP ratio, we need to look to history to understand how our ancestors have done it. An article by The Atlantic summarizes why the US debt-to-GDP ratio fluctuated over time. The common reasons for the decline in public debt as a share of GDP included economic growth, the initiation of new taxes, inflation, and in some eras, a focus on the repayment of debt. The post-World War 2 period differs from the pre-World War 2 period as the government after World War 2 as the government never tried to pay down much of its debts.

While initiating new taxes, creating economic growth, and finding surplus money to repay debts is difficult, inflation looks to be the most reliable way for the government to fight inflation. Inflation increases the nominal value of GDP, reduces the real value of debt, and increases tax revenues. As long as the US keeps the nominal value of debt steady, inflation will help the government reduce the amount of GDP as a percentage of GDP. The post-World War 2 inflation and other waves of inflation helped the US reduce the debt-to-GDP ratio from the end of World War 2 to the early 1980s.

Economic growth isn’t reliable unless a major change in policy is made

Discussions surrounding AI and how it can be a productivity accelerator sparks optimism for economic growth in the US. While economic growth helps reduce public debt as a percentage of GDP, if government spending continues to outpace the revenue gains, the debt burdens will only get bigger.

If the US wants to promote economic growth, it should consider cutting off subsidies to unproductive businesses and allow the Federal Reserve to increase interest rates. Interest rates and inflation are hot political topics. To reduce inflation, the Federal Reserve should be allowed to raise interest rates without receiving political repercussions. Since 2024 is an election year, politicians will want interest rates to remain low to avoid a recession. Recessions look bad to the party that’s currently dominating the government.

If the Federal Reserve can’t do its job and the US continues to support uncompetitive private businesses, the US economy will be littered with zombie companies. And it is already littered with zombie companies. The zero interest rate policy (ZIRP) after the 2008 financial crisis has fueled the growth of zombie startups. Some of these startups reached profitability after achieving the economies of scale they needed. Tesla and Uber are some ZIRP phenomenons that managed to become profitable and many others, like those electric scooter rental companies and WeWork, collapsed.

By letting unviable, debt-laden "zombie" companies fail rather than propping them up with government support or easy credit, the economy becomes healthier. The collapse of zombie companies clears the way for more productive and innovative companies to emerge and thrive. All the capital, labor, and other resources that were once tied to these zombie companies can get reallocated to nimbler, higher-potential businesses. At the same time, letting zombie businesses collapse creates a stronger incentive for businesses to make better decisions. The short-term disruptions caused by the collapse of uncompetitive businesses ultimately strengthen the foundation of the economy by ensuring that capital, labor, and other resources are directed toward their most valuable uses.

I discuss the need for the US to root out zombie companies because Japan, a country with a debt-to-GDP ratio above 200%, couldn’t rely on economic growth to escape this issue. No matter how great Japan is at making electronics and cars, its economy has grown sluggishly since the 1990s. The number of zombie companies in Japan recently swelled to an 11-year high. As the article notes “An increase in zombie companies can hamper the rise of new businesses, holding down wages and hindering workers from moving into growth industries.” If Japan had halted the abundance of subsidies it gave to those zombie companies and allowed the BOJ to let interest rates soar, then it would have a stronger economic foundation, and the country would have a lower public debt burden today.

Back to the 12%

As discussed in the beginning, what are the 12% of simulations that Bloomberg Economics ran that show the US debt-to-GDP ratio on a sustainable path?

While the article doesn’t dive deep into it, the Treasury chief, Janet Yellen, has a view on it. She says the public debt issue is sustainable if the inflation-adjusted interest expense remains below 2% of GDP. In 30% of the simulations, the US inflation-adjusted interest expense goes above 30% over the next 10 years. This creates a case for optimism as 70% of the simulations show the US inflation-adjusted interest expense being below 2% of GDP, making public debt sustainable in the eyes of Yellen.

Other ways that the simulations can show the US debt-to-GDP ratio on a sustainable path include having higher projected economic growth, reduction in government spending, tax increases, and declining interest rates. Out of all these factors, the factor that surprises me most is the reduction in government spending. It’s rare to find a researcher that projects the US government to have lower fiscal spending. When looking at the CBO’s outlook for 2024-2034, the CBO notes that “[t]he biggest factor contributing to smaller projected deficits is a reduction in discretionary spending stemming from the Fiscal Responsibility Act and the Further Continuing Appropriations and Other Extensions Act, 2024.” These acts limit most discretionary funding in the federal government.

Interest rates, while many will say the government should’ve refinanced their debt during the ZIRP era, won’t solve the public debt sustainability issue. The scale of public debt in the economy is large and the larger the scale of debt, the more sensitive the US government is to changes in interest rates. The government should not learn to rely on low interest rates to survive. Even if interest rates remain low, having a large amount of debt will mean the government has to pay more in interest, which does not make the situation more sustainable in any way. Higher interest rates will incentivize fiscal responsibility. How the government finds its way out of the mountain of debt it holds is the question.

Conclusion

The future of the US debt-to-GDP ratio looks risky. While 88% of the simulations done by Bloomberg Economics predicts the ratio will keep going up over the next 10 years, at least we know that in 12% of the simulations show the ratio stabilizing or going down.

How could that happen? A few things could make that possible - the economy grows faster than expected, bringing in more tax money for the government. The government could also spend less money, especially on things like the military and government programs. Taxes could be raised to bring in more revenue. And if interest rates stay low, the government wouldn't have to pay as much to borrow money.

The key is that the government can't just rely on low interest rates to fix the debt problem. Even with low rates, the debt is so huge that it's very sensitive to any increases and the interest expense is already huge on its own. The government will need to make some tough choices, like cutting spending or raising taxes, to get the debt under control.

It won't be easy, but this article shows there's still a chance the U.S. can get its fiscal house in order. This country's leaders need to act now before a crisis forces their hand. The future of the economy is at stake.

Don’t forget to subscribe!